TSMC: 7nm Now Biggest Share of Revenue

by Ian Cutress on January 17, 2019 9:00 AM EST- Posted in

- Semiconductors

- TSMC

- 7nm

- CLN7FF

- Revenue

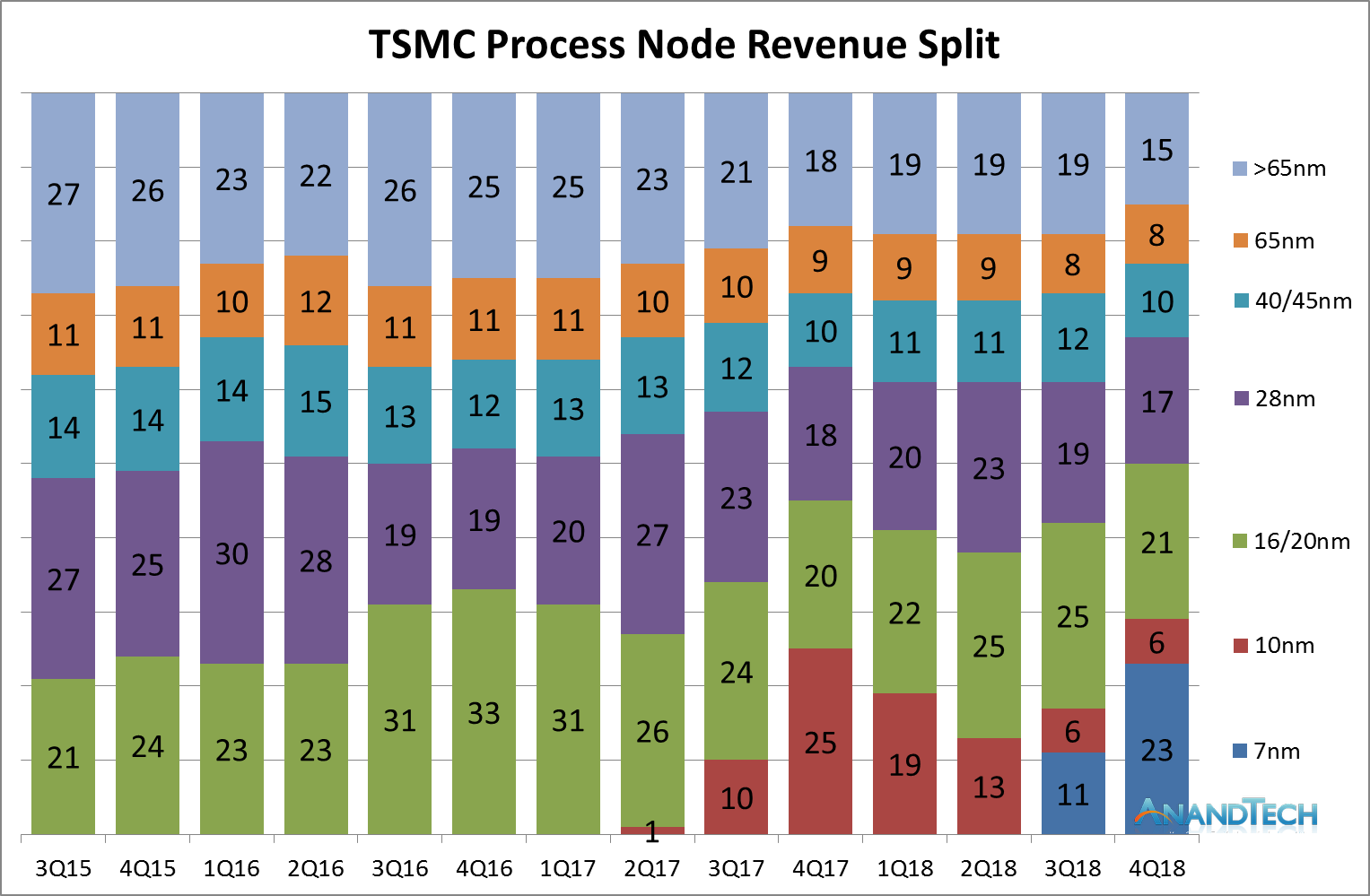

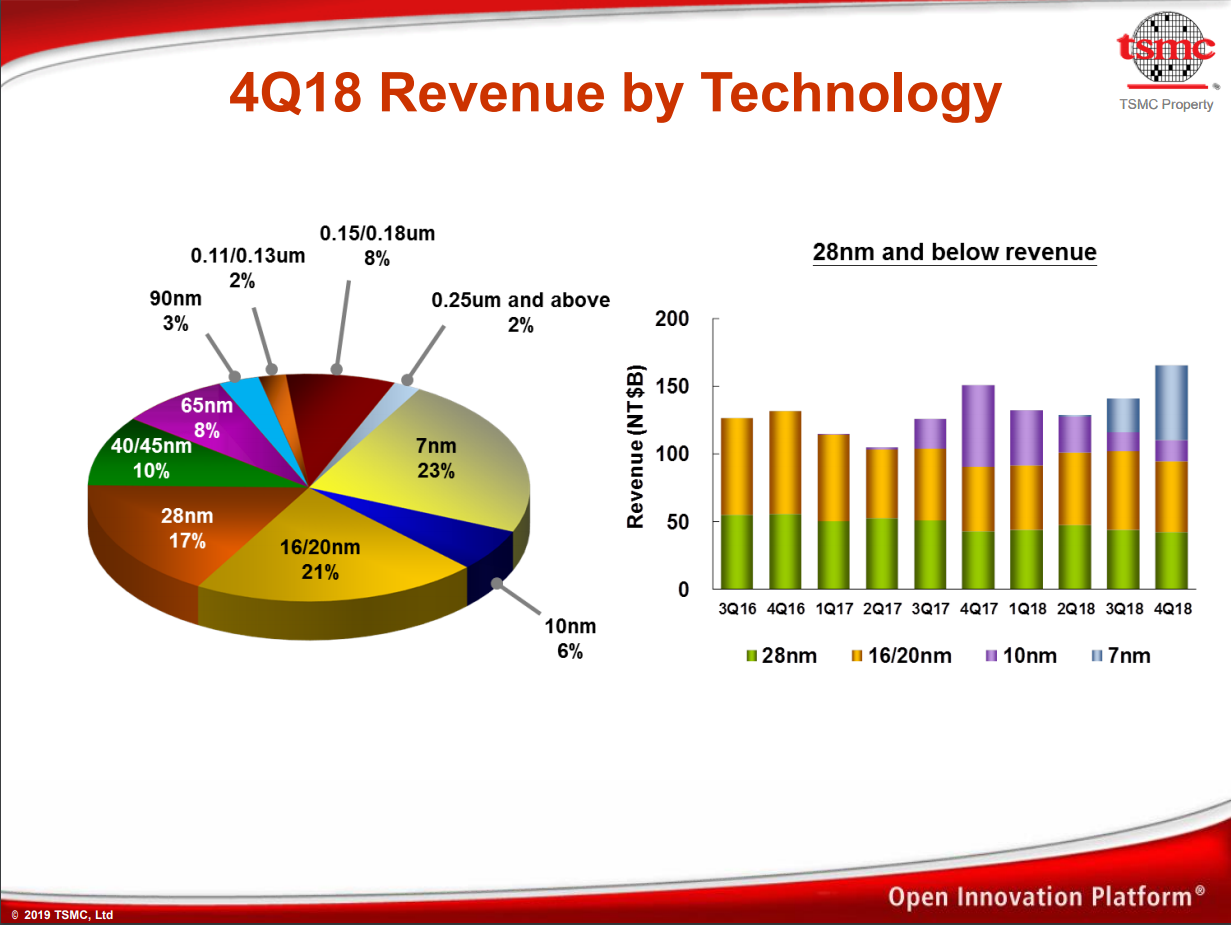

As process node technology gets ever more complex, it costs big dollars to develop and then building chips on the process is also a very costly process. The big foundries often have many process nodes running in parallel across a wide range of price brackets in order to both diversify the revenue streams but also offer multiple competitive options for the market. The latest numbers out of TSMC are stating that in Q4, the revenue generated from their leading edge 7nm node family now takes the biggest percentage of revenue for the company.

As posted by David Schor of WikiChip over Twitter, taking data from TSMC’s earning calls over the years and adding its latest Q4 results to the mix, it shows that 7nm has had a significant ramp, becoming 23% of the revenue of the company since it starting offering it as a process. Over the course of 2018, TSMC has stated that 7nm has accounted for close to 10% of total revenue, and the company expects the process node to be worth ‘greater than 20%’ of its 2019 revenue.

In the Q3 earnings call, CC Wei from TSMC stated that:

This is the first time in the semiconductor industry the most advanced logic technology is available for all product innovations at the same time. We continue to work with many customers on N7, N7+ product design and expect to see more than 100 customer product tape-outs by end of 2019 expect 7-nanometer to be a multiple waves of customer adoptions.

Trendforce has reported that TSMC held 56.1% of the worldwide market share for semiconductor foundry business in the first half of 2018, prior to 7nm being offered. Compared to other foundries, the same report has that GlobalFoundries holds 9.0% of the market, UMC at 8.9%, Samsung at 7.4%, and SMIC at 5.9%; all other players are sub 2.5%. It will be interesting to see if 7nm changes this balance.

On the future of 7nm offerings, back in August 2018, GlobalFoundries announced that it has stopped all 7nm development, that it no longer has plans to develop a 7nm process, and will focus on its current profit-generating technologies such as 14LPP, 12LP, 22FDX, and 12FDX. Also, Samsung’s 7nm offerings are starting to come online and the company has been particularly aggressive about discussing future process node technologies. We have also reported on TSMC's future plans, such as offering 5nm volume production by early 2020.

44 Comments

View All Comments

name99 - Friday, January 18, 2019 - link

And you think TSMC wasn't aware of this dynamic?Especially since they went through the exact same thing with 20nm?

What I see when I read these discussions of "short nodes" is people who desperately want to find SOMETHING to criticize in TSMC's execution, and who latch onto an idiotic point for idiotic reasons.

Dvgeniy - Saturday, January 19, 2019 - link

Are you ever reading/joining their quarterly calls? They openly communicate that not all their expectations always maturalize. It was during the last call, and the same was a year ago. Short nodes are good for the progress, but they are not making much money on those.Dvgeniy - Saturday, January 19, 2019 - link

*materializename99 - Saturday, January 19, 2019 - link

Like I said, some nodes are the scaffolding that makes the other nodes possible...Or, if you want a different analogy, some nodes are the loss-leader movie, but they make it up in merch and foreign distribution.

You have to look at the ENTIRE picture. No-one wants to lose money on a node (and I don't believe they ever do). But not all nodes are there to be cash cows; and as long as they do their job of moving the company onward to the next cash cow, everyone's happy --- including the INTELLIGENT analysts and investors.

You can always find some idiot complaining about the financial performance of one node; the question is --- why is that idiot worth listening to?

eva02langley - Thursday, January 17, 2019 - link

Intel is really in trouble... there is no way in hell they will keep their fabs.SquarePeg - Thursday, January 17, 2019 - link

I keep expecting to see an announcement that they are going to break ground on a new fab or two and open up their process to third parties in an effort to cover R&D costs and generate additional revenue.FunBunny2 - Thursday, January 17, 2019 - link

it's worth noting that 4/17 10+7 is not much smaller than they became in 4/18. also, isn't 7nm generally considered just 10nm over most of the real estate on a SoC?Dvgeniy - Thursday, January 17, 2019 - link

A12 have 60% more transistor than A11. And all with a smaller die size!tommybobberson - Friday, January 18, 2019 - link

What about Intel, what share of the market does it hold?Kvaern1 - Friday, January 18, 2019 - link

https://www.statista.com/statistics/294804/semicon...